Monthly GDP estimates measure a sharp decline in latest construction output figures seeing largest month-on-month drop in growth since June 2012

The new construction output figures published by the ONS show a mixed picture for the industry:

- The all work series decreased by 0.3% in Quarter 4 (Oct to Dec) 2018, following an increase of 2.1% in Quarter 3 (July to Sept) 2018; this decrease was driven by repair and maintenance output, which was down by 2.8%.

- The decline in repair and maintenance was caused by drops in private housing and non-housing repair and maintenance output of 4.0% and 2.9% respectively.

- These falls were offset somewhat by a 1.1% increase in all new work, driven by increases of 1.9% in infrastructure and 1.4% in private commercial new work.

- The monthly series saw a sharper decline, with the all work series in December 2018 decreasing by 2.8% below the level seen in November 2018; this is the largest month-on-month fall in growth for all work since June 2012, when the series dropped by 4.3%.

- When compared with 2017, the level of all work in 2018 saw a 0.7% increase; this was the lowest annual growth since 2012, which saw a 6.9% decrease in annual output.

A large positive contribution from the services sector was partially offset by smaller negative contributions from the production and construction sectors.

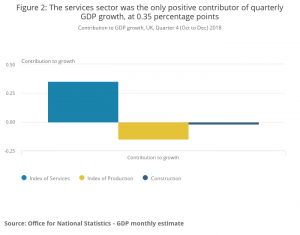

The services sector was the only positive contributor of quarterly GDP growth, at 0.35 percentage points

Growth in the services sector was 0.4% in Quarter 4 (Oct to Dec) 2018. Meanwhile, the production industries contracted by 1.1% and construction contracted by 0.3%. These growths mean that the services sector was the only positive contributor to gross domestic product (GDP) growth in Quarter 4, while the other two sectors had negative contributions.

Construction growth contracted in Q4 2018, the first negative three-month growth since May 2018

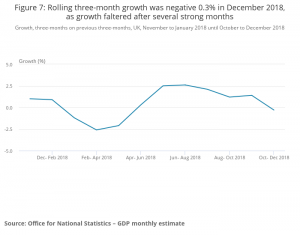

Rolling three-month growth was negative 0.3% in December 2018, as growth faltered after several strong months growth, three-months on previous three-months, UK, November to January 2018 until October to December 2018

Rolling three-month estimates are calculated by comparing GDP in a three-month period with GDP in the previous three-month period, for example, GDP in October to December compared with the previous July to September.

Rolling three-month growth was 0.2% in December 2018, as the slowdown from a peak in August continued.

Construction contracted by 0.3% in Quarter 4 (Oct to Dec) 2018. Although new work grew on the quarter, this was offset by a fall in repair and maintenance.

Monthly growth in construction was negative 2.8% in December 2018, with both new work, and repair and maintenance contracting in this period.

Rob Kent-Smith, Head of GDP commented: “Declines were seen across the economy in December, but single month data can be volatile meaning quarterly figures often give a better indication of the health of the economy.

“The UK’s trade deficit widened slightly in the last three months of the year, while business investment again declined, now for the fourth quarter in a row.”

GDP fell by 0.4% in December 2018

Month-on-month gross domestic product (GDP) growth was 0.2% in October and November 2018. However, monthly growth contracted by 0.4% in December 2018. The last time that services, production and construction all fell on the month was September 2012.

Monthly GDP estimates are much more volatile than quarterly GDP estimates, with almost one in every four months in the past 21 years showing negative GDP growth.

Therefore, monthly estimates should be used alongside other measures such as the three-month growth rate when looking for an indicator of the longer-term trend of the economy. However, they are useful in highlighting one-off changes that can be masked by three-month growth rates.

Clive Docwra, Managing Director of McBains said: “Today’s figures show a mixed picture – unsurprising given concerns about the UK economy and whether it can withstand a no-deal Brexit.

“These fears, coupled with longer running issues such as high import costs and skilled worker deficits, are now cutting through and impacting key investment decisions.

“To turn the corner, the industry needs confidence and the support of the Government. The Brexit uncertainty will need clarifying soon if the sector is to push on and build the homes our country needs.”