The analysis shows that infrastructure was the biggest workhorse for the industry in 2024, but new housing applications did not grow despite Labour’s promises

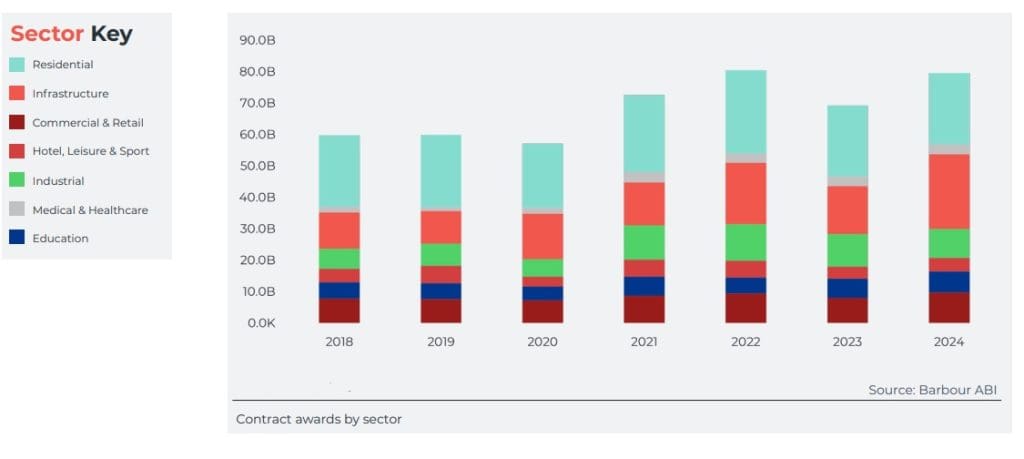

The Barbour ABI January analysis shows contract awards in 2024 rising to £79.5bn.

The largest gain by region saw the East of England which grew by 52%. This growth is unexpected after the worrying trends in the previous analysis.

The North East fell by 20%

The Barbour ABI January analysis looks at seven primary sectors in the construction industry, including:

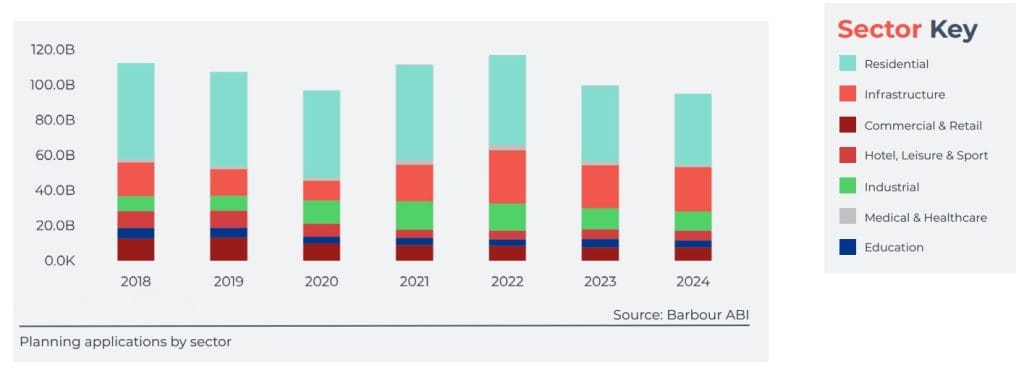

- Residential: Includes private developments, housing associations, apartment blocks, retirement homes, halls of residence, hostels, and barracks. Residential developments are a key driver of growth, with high contract awards in London and the Republic of Ireland. Top contract award regions include the Republic of Ireland (£472M), London (£470M), and the East of England (£299M). Top planning approval regions include the North West (£1.04B), Republic of Ireland (£649M), and the South West (£527M)

- Commercial & Retail: Covers offices, shopping centres, food retailing, general retail, retail warehouses, and garden centres. Commercial sector evolution is impacted by changing office space demands and the decline of traditional High Street retail. Top contract award regions include London (£627M), Yorkshire & Humber (£95M), and the South East (£42M). Top planning approval regions include London (£249M), the North West (£187M), and the South East (£80M).

- Infrastructure: Encompasses transport, civic & public works, utilities, and civil engineering. Infrastructure projects remain dominated by large government and utility projects, requiring partnerships with major contractors. Top contract award regions include Yorkshire & Humber (£521M), the South West (£518M), and the Republic of Ireland (£134M). Top planning approval regions include the East of England (£835M), the East Midlands (£775M), and Scotland (£466M)

- Industrial: Includes heavy and light industrial, food production, cold stores, warehouses, laboratories, and agricultural buildings. Industrial sector benefits from increased demand for warehousing due to e-commerce expansion. Top contract award regions include Yorkshire & Humber (£156M), the South East (£141M), and the South West (£116M). Top planning approval regions include Yorkshire & Humber (£680M), the South West (£642M), and the East of England (£161M)

- Education: Covers nurseries, primary and secondary schools, private schools, colleges, universities, and special education institutions. Education sector investments continue, although not as consistently high as other sectors. Top contract award regions include London (£153M), Scotland (£59M), and the North West (£50M). Top planning approval regions include the South West (£55M), Scotland (£47M), and the North West (£43M)

- Hotel, Leisure & Sport: Includes hotels, motels, pubs, restaurants, leisure centres, arenas, stadiums, exhibition centres, and community centres. Hotel, leisure, and sports developments remain active, with London leading in planning approvals. Top contract award regions include the West Midlands (£78M), Scotland (£50M), and London (£47M). Top planning approval regions include London (£1.2B), the Republic of Ireland (£115M), and the West Midlands (£77M)

- Medical & Healthcare: Covers public and private hospitals, hospices, psychiatric and nursing homes, surgeries, and veterinary services. Healthcare sector opportunities are expected to grow due to government-backed hospital refurbishment and construction projects. Top contract award regions include the South East (£34M), the South West (£26M), and the North West (£14M). Top planning approval regions include the Republic of Ireland (£25M), London (£24M), and Yorkshire & Humber (£16M)

Infrastructure drove growth in 2024

Green initiatives, in particular, drove infrastructure growth, which may have led to a strong 56% growth, but may also be symptomatic of industry issues. Housing activity grew by just 1%, and industrial spending dropped by 12%.

Planning approvals also dropped by 8%, dipping below £100bn for the first time since 2022. Amidst the Labour drive for new housing, these are concerning figures.

Barbour ABI head of business and client analytics, Ed Griffiths, said: “Despite the headline growth, not all is as it seems. Infrastructure has been carrying the rest of the industry on its back in 2024. Without these projects, growth would be in the single digits.

“Rising costs, market uncertainty, and skilled labour shortages continue to plague the industry. Insolvencies, including the collapse of major contractors like ISG, have delayed key projects and created ripple effects across the sector. High interest rates have further discouraged investment, reducing demand for new homes and stalling large developments.

“Labour’s planning reforms offer hope to housebuilders, but the industry is holding its breath to see if these changes will lead to a rise in applications for new builds in 2025. In the meantime, we’re looking to emerging sectors like data centres, spurred by Keir Starmer’s recent AI investment announcements, to carry growth in the year ahead.”