The statistics show that after a mild increase in Q4 2024, construction output then fell again

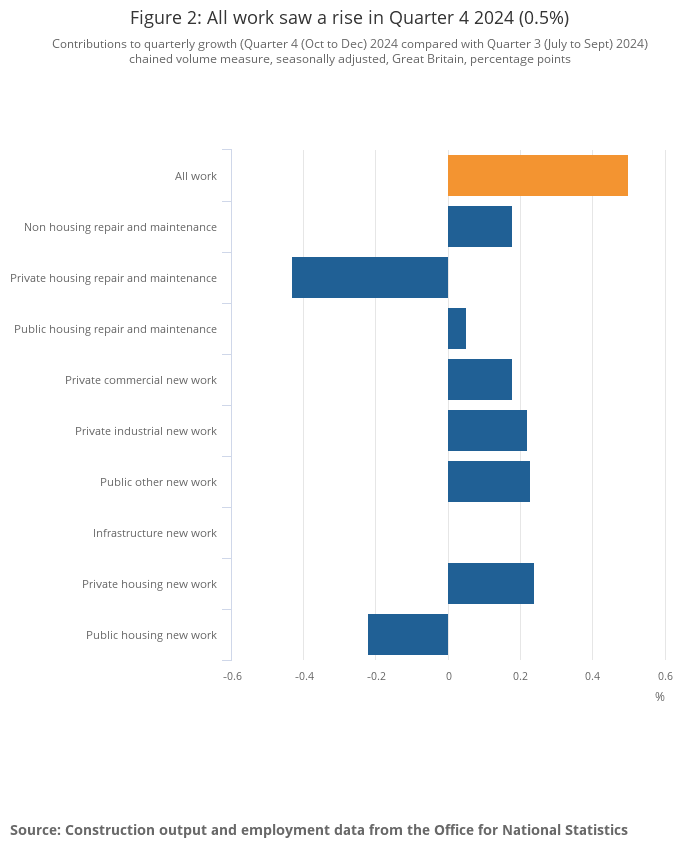

In October-December 2024, construction output was estimated to have increased by 0.5% on Q3, due to a 1.2%, according to ONS stats Q4 2024.

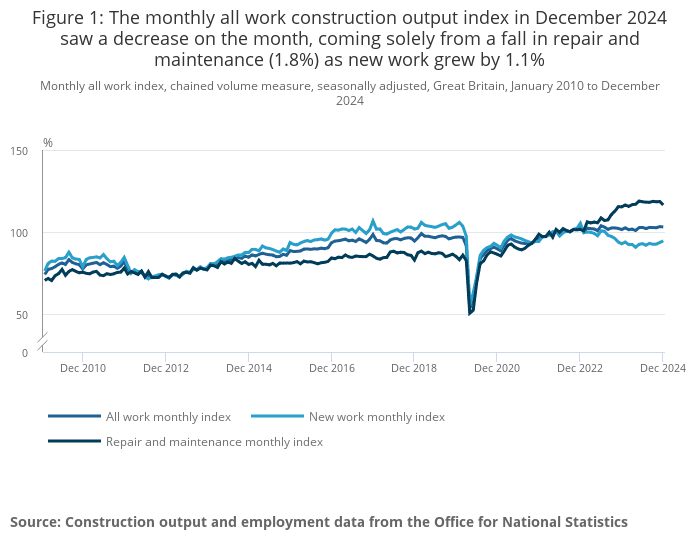

Since then, construction output volume has fallen by 0.2% in December 2024 due to a further drop in repair and maintenance.

Five of the nine sectors fell in December

The key contributors to the fall were non-housing repair and maintenance, and private housing repair and maintenance, falling by 1.8% and 1.4%.

Total construction new orders fell by £231m, or 2.4%, in Q4 2024 from the last quarter, solely due to a fall of 23.5% in infrastructure new work and 19.7% in private industrial new work.

Year-on-year, the construction output total increased by 0.4% in 2024, marking the fourth year of annual growth in a row.

This is due to the rise of repair and maintenance by 8.5% counter-acting the decrease in new work by 5.3%.

By sector, four of the nine sectors saw an increase in annual growth, with non-housing repair and maintenance, and private housing repair and maintenance growing by 8.5% and 7.0% respectively. Infrastructure new work fell by 9.3%.

Industry reacts to ONS stats Q4 2024

Gareth Belsham, director of Bloom Building Consultancy, said: “Construction lurched rather than limped across the finish line at the end of 2024. After flatlining in October, jumping in November and then shrinking in December, total output across the industry was mixed.

“But for all the monthly volatility, momentum remains. In 2024, as a whole, the industry grew by 0.4% compared to 2023, chalking up a fourth consecutive year of expansion.

“However, question marks linger about how resilient the growth is. More than half of the nine subsectors tracked by the official data contracted in December.

“Of far greater concern is the continued slowing of the new orders pipeline. The total value of orders placed in the final quarter slumped by 2.4% compared to the preceding three months. It now stands at the lowest level seen since the shutters came down on much of the UK economy during the first Covid lockdown of 2020.

“The fact that the Q4 slowdown in orders coincided with the Chancellor’s bearish Budget will make awkward reading in 11 Downing Street, but the decline began long before that. New orders shrank by nearly a quarter in the third quarter, suggesting that the fragility of business sentiment has deeper roots.

“Yet there are bright spots. Orders for private sector housebuilding surged by 24% in the final quarter of the year, as residential developers who held off for much of 2024 decided to pull the trigger on previously paused schemes.

“Meanwhile commercial property builders ended the year on a high. The value of commercial orders placed in the final quarter was 15.1% higher than in the same period in 2023, and orders surged by 16% in 2024 as a whole.

“The industry has begun 2025 finely poised. The Chancellor is making all the right noises about construction being an engine of wider economic growth and the prospect of falling interest rates will make it easier for developers to buy land and get building.

“For all the momentum, business sentiment is patchy and developers, landlords and investors are laser-focused on value and proceeding with caution.”

Clive Docwra, managing director of property and construction consultancy McBains, said: “There will be little surprise among the industry that December witnessed a fall in output, given the ups and downs of the previous eleven months.

“Despite the disappointing December return, the industry will take heart that new work orders actually grew during the month, but more importantly, the fourth quarter of 2024 saw half a percentage rise in output, which is more than perhaps many expected. It means a number of industry sectors will be looking forward with a degree of optimism in the next few months.

“In particular, the recently published planning reforms and falling interest rates will hopefully inject new momentum into the housebuilding sector, although skills shortages and cost inflation on materials could still have an impact on significant growth across work sectors.”

The ONS stats Q4 2024 can be read in full on the ONS website.